Home Mortgage Broker Free Mortgage Broker Business Plan 8.1 Financial Statement Analysis

8.1 Financial Statement Analysis

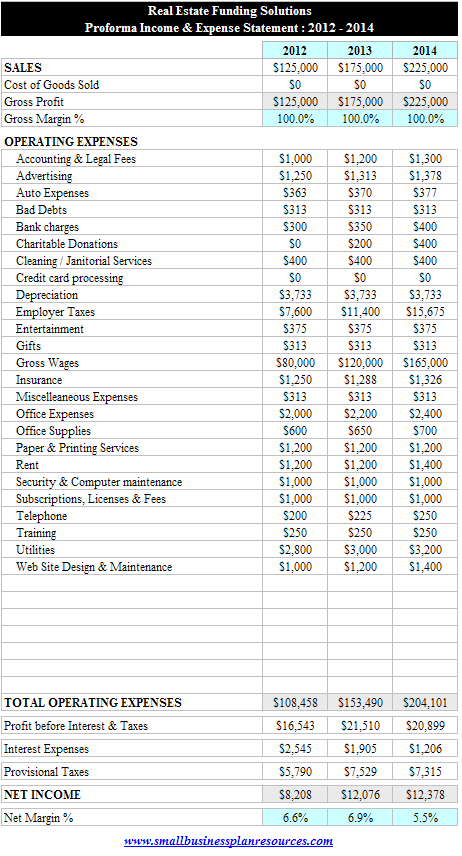

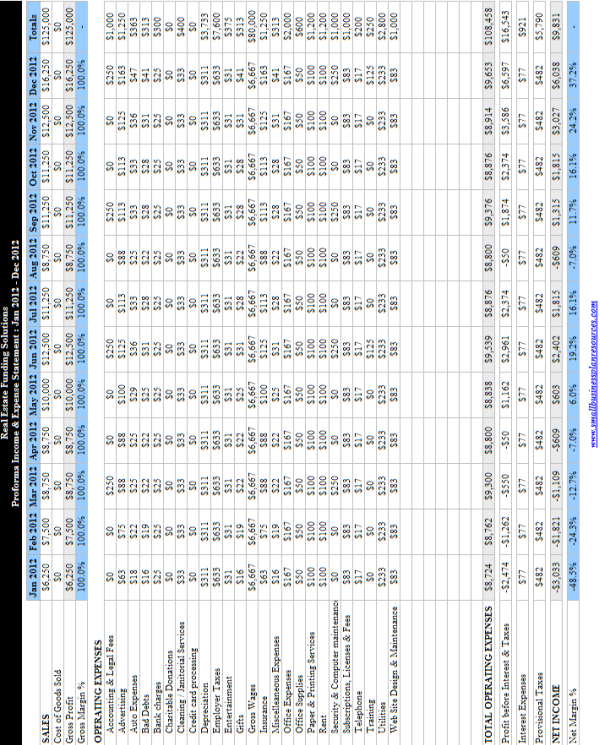

We began by entering in our sales projections that we had arrived at earlier in Section 5.7, 5.8 and 5.9 into the modules. Thus we start with our sales projections of $1,25,000 for year 1, $175,000 for year 2, and $225,000 for year 3 respectively. As you know from our sales forecasting sections there are three possible economic scenarios that we considered when looking at sales forecasting - the slow market, the good or normal market and the great market. We decide to go with the good or normal market condition numbers in our financial modules since it presented the middle of the road approach towards projections which we felt was appropriate.

We began by entering in our sales projections that we had arrived at earlier in Section 5.7, 5.8 and 5.9 into the modules. Thus we start with our sales projections of $1,25,000 for year 1, $175,000 for year 2, and $225,000 for year 3 respectively. As you know from our sales forecasting sections there are three possible economic scenarios that we considered when looking at sales forecasting - the slow market, the good or normal market and the great market. We decide to go with the good or normal market condition numbers in our financial modules since it presented the middle of the road approach towards projections which we felt was appropriate.

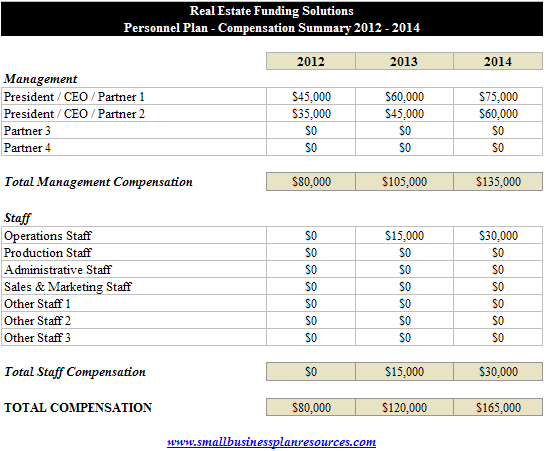

Compensation Forecast:

In our compensation forecast, we are projecting that Ryan who owns a larger share of the company will be drawing a salary of $45k, $50k and $75k in the first, second and third year respectively. David who has a smaller share of the company is projected to draw a salary of $35k, $40k and $60k during the first three years of operations. Both the partners have good personal balance sheets and understand that their business is a pay for performance business - if business is slow, they will have to lower the amount of salaries they give themselves and vice versa.

The largest operating expense for a small business like Real Estate Funding Solutions is of course compensation. Given that both the owners have no plans of hiring any staff until the second year of operations, the only compensation expense in the first critical year of operations will be the salaries that they pay themselves over which they have complete control.

Capital Contributions:

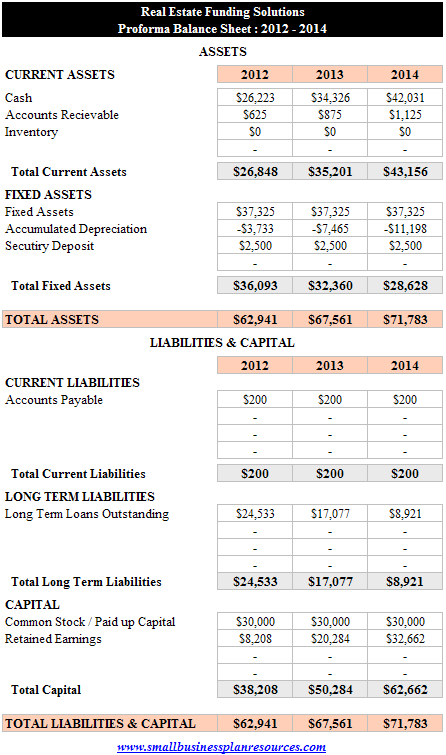

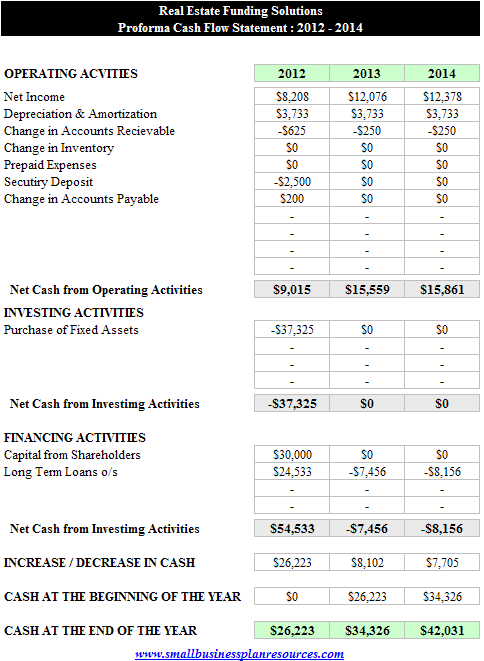

The initial capital contribution at the outset will be a total of $30,000. Ryan will be making 75% of the total contribution by bringing $22,500 to the table. David will be responsible for the remaining $7,500 representing the remaining 25%. Both the partners don't think that they will need to make any additional contribution to the business, but they are ready, willing and able to do so if the need were to arise.

Loan & Interest Expense Summary:

We will be taking out a private party fully amortizing loan where we will be paying back both principal and interest on the loan every month. We have anticipated that a loan in the amount of $11,350 at 9% interest for 4 years should do the job for us and we are projecting that we will be putting in for this loan at the outset.

As we keep paying this loan down, we anticipate that the at the end of each year we will have the following projected principal balance outstanding - $8,882, $6,182 and $3,230 for 2012, 2013 and 2014 respectively.

Fixed Asset & Depreciation Summary:

The fixed assets that we have entered in for 2012 includes the upfront capital improvements to the location, along with all the other fixed assets like furniture & fixtures, computer hardware & software, printers, security systems, deposit etc that we will need to run the business for the next three years. We don't anticipate adding any more to our existing fixed asset infrastructure unless one of the pieces of equipment goes bad - even in that instant, our product warranties should be enough to cover the contingencies.

Purchases, Inventory & Cost of Goods Sold:

In this section we simply enter in the cost of goods sold for each year along with the changes in inventory if any. The projectedcost of goods sold in our case will be $0 since there no intrinsic cost of production for any of our services. This is fairly common for service oriented businesses like Real Estate Funding Solutions. Also very common in the service business is the lack of any inventory. Typically service businesses don't have any tangible physical inventory they carry and hence the inventory numbers for all three years of operations are projected to be at $0.

Accounts Receivable Summary:

In the real estate financing business, there tend to be very low accounts receivables, but there are certainly occasions when a borrower does not fulfill their promises of sending in the cost of the application or processing fees. Sometimes, in the event of clerical errors, when an appraiser or title company owes us a refund, they fail to send the check in. Hence we are projecting that accounts receivables for each of the three years will be 0.50% of sales.

fulfill their promises of sending in the cost of the application or processing fees. Sometimes, in the event of clerical errors, when an appraiser or title company owes us a refund, they fail to send the check in. Hence we are projecting that accounts receivables for each of the three years will be 0.50% of sales.

Accounts Payable Summary:

Likewise, it is rare to have large accounts payable in a service oriented business like Real Estate Funding Solutions. There may be occasions when we have to return a small portion of the application or processing fees, or have to pay a vendor like an appraiser or title company a fee that we failed to adequately collect from our borrower - to account for all this we are projecting a modest accounts payable for $200 for each of the three years.

Security Deposit:

A security Deposit in the amount of $2,500 is what we anticipate paying our landlord and that security deposit will of courseremain with the landlord for the duration of the three years that are being projected here.

Quick Links:

- Go to the Corresponding Template section for this industry.

- Go to the Corresponding Questionnaire section for this industry.

Small Business Owner Resource Center

Articles on the Small Business Financing Sources, the Small Business Loan Basics, small business loans Checklist and SBA Loans are incredible sources of knowledge for the small business owner.

Credit Report and Credit Score Analysis, how to Read a Personal Credit Report and all about Business Credit cover the intricacies of credit and are required reading for everybody.

The Foundation Grant Directory is a free listing of sources for grants by state. Why not look if there is some free money out there for your business. Hey - you never know!

The Business Loan Application covers every item you will need in your loan package and tells you how to get approved for business loans.

Fire your loan broker and use our Free Business Loans Bank / Lender Directory to find every bank in the country lending to small businesses.

If you are looking to start a business - look no further. Check out the Free Incorporation Guide discussion and the State Incorporation Resource Directory.