Home Financing Personal Credit and Business Credit Credit Report and Credit Score Analysis

Credit Report and Credit Score Analysis

4. Difference in credit scores

The credit score that is used to underwrite and approve loans for a borrower is know as the representative credit score and this is the middle score when three scores are reported; or the lower score when only two scores are reported. For business loan applications, most lenders will request in-file merged credit reports which will have data from at least two of the three repositories. While for the most part the data reported by to each of the three repositories is the same, it is very often the case that the credit history of one account is reported to only one or two of the three repositories. In order to protect their interests, bankswill look at the credit history for a potential borrower being reported to call three of the repositories. They may however choose to go with the credit score of any one of the three repositories or the highest of all three and as in the case of residential mortgages, the lowest of all three scores being reported.The reason that the credit scores reported by each of the three repositories can be different is that they may have different information on you or it may be because the way they compute credit scores is different. Each company uses it’s own algorithms to compute credit scores and it is generally understood that these algorithms are developed by the Fair Issac Company for each repository. View our sample credit report to see how information is reported.

5. Will credit scores drop when they run credit?

The chances your credit score will drop because of one inquiry into your credit are slim. However repeated inquiries from different lenders against your credit is viewed as a negative. Generally the repositories understand that you are shopping for credit when looking for say a business loan or auto loan, thus if your inquiries all take place within a few days of each other, they will affect your credit scores negatively less than if they are spread out over many weeks. We highly recommend that if you are applying to multiple lenders for a business loan that you apply concurrently if possible. If you have found out from a lender that your score is on the border line, then stay away from further applications for credit.

6. Calculation of Credit Scores

Although many types of credit scoring models exists, a model developed by Fair, Issac & Company Inc. is the one that is used by the three repositories to obtain credit scores after evaluations of the following:

Number and age of accounts: The scoring models consider a credit history that consists of older, established accounts as representing a lower risk. However, they do not automatically consider a newly established credit history as a higher risk since other lower-risk factors in the borrower's credit report may offset the risk of the less established credit history.

Important to note here is the fact that older accounts with established credit history are given more weight in the scoring models than the newer accounts. Thus if you are contemplating shutting down a credit card that has been around for more than 48 months – don’t do it. One account history of that length will be better than 2 to 3 accounts opened recently.

Payment History: The scoring models consider the borrower's payment history as a significant factor in determining the credit score. The type of information that is evaluated includes data on late or missed payments; public record and collection items; the frequency, recent, and severity of any delinquent payments (including identifying any occurrences of 30, 60, or 90days past-due payments as being frequent occurrences or isolated incidences); and the presence of bankruptcies, foreclosures, outstanding liens, or judgments. Take a look at our sample personal credit report for an illustration of how the payment histories show up on a credit report.

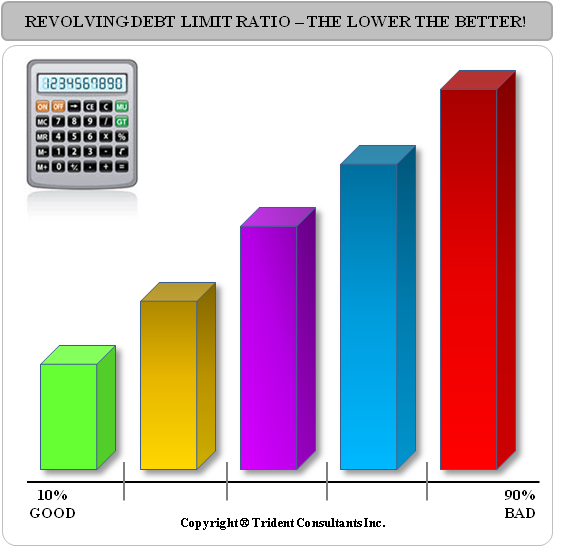

Utilization of Credit: The models here take into account the total amount of lines of credit that the borrower has opened against his name and also the amount of the actual line that he had drawn down and is being reflected in the outstanding balance on the account. Clearly the more accounts a borrower has open with lines drawn down the more it will impact his credit negatively. It is recommend that if you are getting ready for a business loan you should order your own credit report at least 3 months ahead of time and get a good look at all items that are being reported. If you find that you have one credit card that is close to be ‘maxed out’, in order words it has a balance outstanding of almost the entire credit limit, you should transfer some of those balances to other cards. Lenders do not like to see lines being used close the maximum limit. As a general rule it is recommend that no more than 65% of each credit line be used. The ratio that lenders look at when studying your credit report is revolving debt to limit ratio – that is the total debt you have outstanding compared to what is available to you.

Small Business Owner Resource Center

Articles on the Small Business Financing Sources, the Small Business Loan Basics, small business loans Checklist and SBA Loans are incredible sources of knowledge for the small business owner.

Credit Report and Credit Score Analysis, how to Read a Personal Credit Report and all about Business Credit cover the intricacies of credit and are required reading for everybody.

The Foundation Grant Directory is a free listing of sources for grants by state. Why not look if there is some free money out there for your business. Hey - you never know!

The Business Loan Application covers every item you will need in your loan package and tells you how to get approved for business loans.

Fire your loan broker and use our Free Business Loans Bank / Lender Directory to find every bank in the country lending to small businesses.

If you are looking to start a business - look no further. Check out the Free Incorporation Guide discussion and the State Incorporation Resource Directory.